Taxpayers May Have Been Overcharged Up To €500 On Their Income Tax Since 2016

Finance Minister Clyde Caruana has acknowledged that there is a discrepancy between the amount of tax being paid by workers earning above a certain threshold and the official tax rate, but stopped short of admitting it was a mistake.

According to calculations carried out by Lovin Malta, after consultation with several tax practitioners, single taxpayers earning over €19,500, couples earning over €28,700 and parents paying the single rate whose income exceeds €21,200 are paying a €90, €120 and €105 more than they think they are.

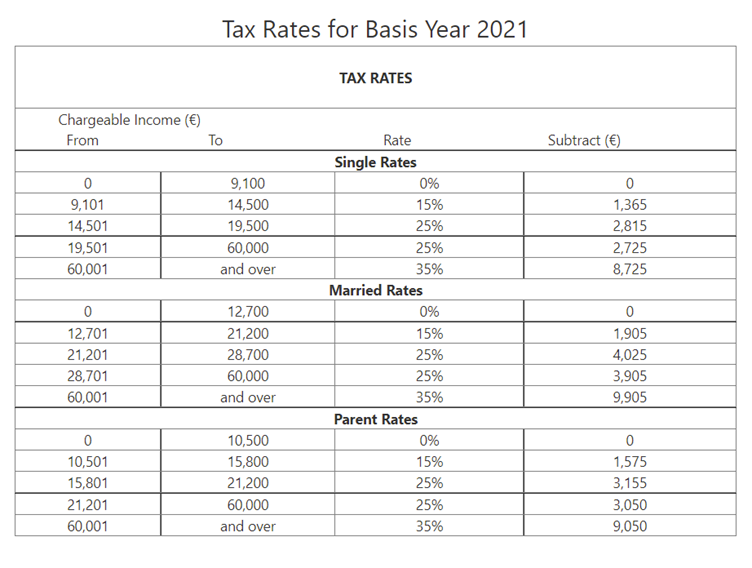

Income tax in Malta is taxed progressively in five brackets, with the first €9,100 being tax-free. Each subsequent bracket is taxed at a different percentage, up to the highest bracket covering earnings over €60,000.

The tax commissioner’s website states that the tax rate on income between €19,500 and €60,000 is 25%, however, if one calculates this according to the specific wording of the law, the amount due works out to a rate higher than 25%.

The difference lies in the method one uses to calculate tax due and relates to the number on the rightmost column of the above table – the ‘Subtract’ column.

The number represents a quicker way of calculating tax by allowing whoever is making the calculation to avoid having to count the tax due in each bracket separately and to instead take the gross income, multiply it by the value in the ‘Rate’ column and deduct the value in the ‘Subtract’ column.

Prior to 2016 – the year the tax brackets were last changed – calculating the tax due “manually” and using the subtraction method would give the same answer. Since 2016, however, the second quicker method gives a higher value than the longer calculation.

PN MP Robert Arrigo had picked up on the change and had warned Parliament in January 2017 that workers were being overcharged on their income tax. He insisted that the government should refund all those affected but his claims were rubbished by a Finance Ministry spokesperson, who insisted that “the 26% tax bracket did not exist”.

Speaking to Lovin Malta, Finance Minister Clyde Caruana refused to acknowledge that the table contained an error.

He pointed to the fact that in 2016, the government had decided to split the 25% tax bracket in order to give a tax break to the lower-earning segment. However, by splitting the bracket, and indicating different amounts to be subtracted, a new bracket was effectively created, with a different tax rate.

Caruana expressed doubts about whether this was the best way of helping specific segments of the workforce, adding that sending a cheque in the post was far more effective.

The explanation, however, does not explain the discrepancy in the tax due when using the two methods, with the minister accepting that taxpayers were, strictly speaking, paying tax at a slightly higher rate than believed and than indicated in the rates column.

The observation has left many tax practitioners, including some working at major local firms perplexed at how what appears to be such a glaring mistake was not noticed earlier.

While a relatively small amount of money, the prospect that taxpayers could have paid an extra €90 in tax every year put the recent tax refunds handed out by the government in a different context.

Mistake enshrined in law

Interestingly, 2016 was also the year that the wording of Malta’s Income Tax Act was changed. While Article 56 previously specified the rates at which income in each bracket was to be taxed, in 2016 the percentage rate was replaced with a specific calculation.

The budget implementation bill that enshrined it in law even specified that the words “is taxed at the following rates” should be changed to “established as follows”.

So instead of a tax rate, which can be easily understood by everyone, the law now includes a seemingly arbitrary calculation.

At a first glance, the wording simply formalises a quick and helpful calculation everyone was using to calculate tax anyway, but it also introduces a greater possibility of mistakes, such as this, being made.

Besides the matter of how such a basic mistake in such a fundamental law was not picked up on before it was tabled in Parliament, it also raises questions about why the need was felt for the wording of the Income Tax Act to be changed.

It is understandable for a tax practitioner to use a calculation summarizing the different bands to save time on workings, but one would expect a law that is applicable to everyone to be written in a clear manner than is understandable by all.

Breaking down the numbers

The amount paid by each worker in income tax is determined by Article 56 of the Income Tax Act on the basis of their gross annual income.

Malta operates a progressive tax system, meaning that higher incomes are taxed at higher rates. To accomplish this, income is divided into bands, and the money earned within each band is taxed at a specific rate.

So, according to (what we believe to be) the present tax rates, someone earning €20,000 a year would expect to pay €2,185 in income tax for a single year – no tax on the first €9,100 earned, €810 on the subsequent €5,400, €1,250 on the €5,000 after that and €500 in the €19,501- €60,000 bracket.

But this isn’t what the law says one should be paying. Sticking to the €20,000 salary example, according to Article 56 of the Income Tax Act:

A person earning €20,000 a year would need to take their gross annual salary and multiply it by 25% before subtracting €2,725, in order to calculate what they owe in tax. But (20000 x 0.25) – 2725 is €2,275, not €2,185.

This means that, according to the law, the effective tax rate on income of between €19,500 and over varies according to one’s income and is significantly higher at the lower end of the salary spectrum.

Rather than subtracting €2,725, the law should state that €2,815 should be subtracted. Similarly, the law should read €8,815 rather than €8,725 in the €60,000+ bracket.

The anomaly is not present when calculating tax due in years preceding 2016, the last year that the tax brackets were changed. It would appear that the change in tax brackets that year led to an error in the values provided by the tax commissioner for the purpose of calculating tax.

So, have people actually been paying more tax?

This is where it starts to get tricky. It is ultimately the law which determines how much tax one must pay and not the minister’s budget speech or a table on the tax commissioner’s website.

One would technically need to read the wording of the law and ensure that the tax paid is worked out accordingly. In reality, income tax payments, especially for workers employed with large companies, are calculated by the company’s payroll system.

Lovin Malta understands that most commonly used payroll system software on the island would base their calculation on the subtraction number.

This means that they calculate tax according to the present wording of the law and the higher tax rate.

What do you make of this? Let us know in the comment section